If you’ve ever wondered why some people say “1 bitcoin buys more, not less, as the years go by,” it comes down to one simple design choice: a fixed supply. Bitcoin’s monetary policy caps total issuance at 21 million coins, released on a predictable schedule that halves new supply roughly every four years. In contrast, fiat currencies like the dollar, euro, or yen expand as central banks and commercial banks create new money to meet policy goals or credit demand. Those two paths—scarcity versus elasticity—lead to very different outcomes for purchasing power.

This article unpacks how Bitcoin’s engineered scarcity can increase purchasing power and make big-ticket items feel cheaper over time, and why fiat money creation tends to erode purchasing power through inflation. We’ll also look at caveats, because reality is messier than a single chart.

Scarcity as a Feature, Not a Bug

The core of Bitcoin’s design is digital scarcity. There will never be more than 21 million BTC. Issuance is algorithmic, not subject to committees, elections, or emergencies. Every ~210,000 blocks (about four years), the block subsidy paid to miners halves. That means the flow of new coins keeps falling until it approaches zero.

Economically, when supply is fixed or very inelastic, changes in demand dominate the price. As adoption grows—more savers, more institutions, more countries experimenting with bitcoin as a reserve—demand pressure tends to push the price of each unit up. If a currency appreciates over long periods, each unit buys more stuff. That’s the essence of increased purchasing power.

Contrast this with fiat, where money supply expands over time. Even at modest growth, compounding means a lot more currency units chasing roughly the same number of goods and services. Unless productivity outpaces money growth by a wide margin, prices drift upward—otherwise known as inflation. The same unit buys less.

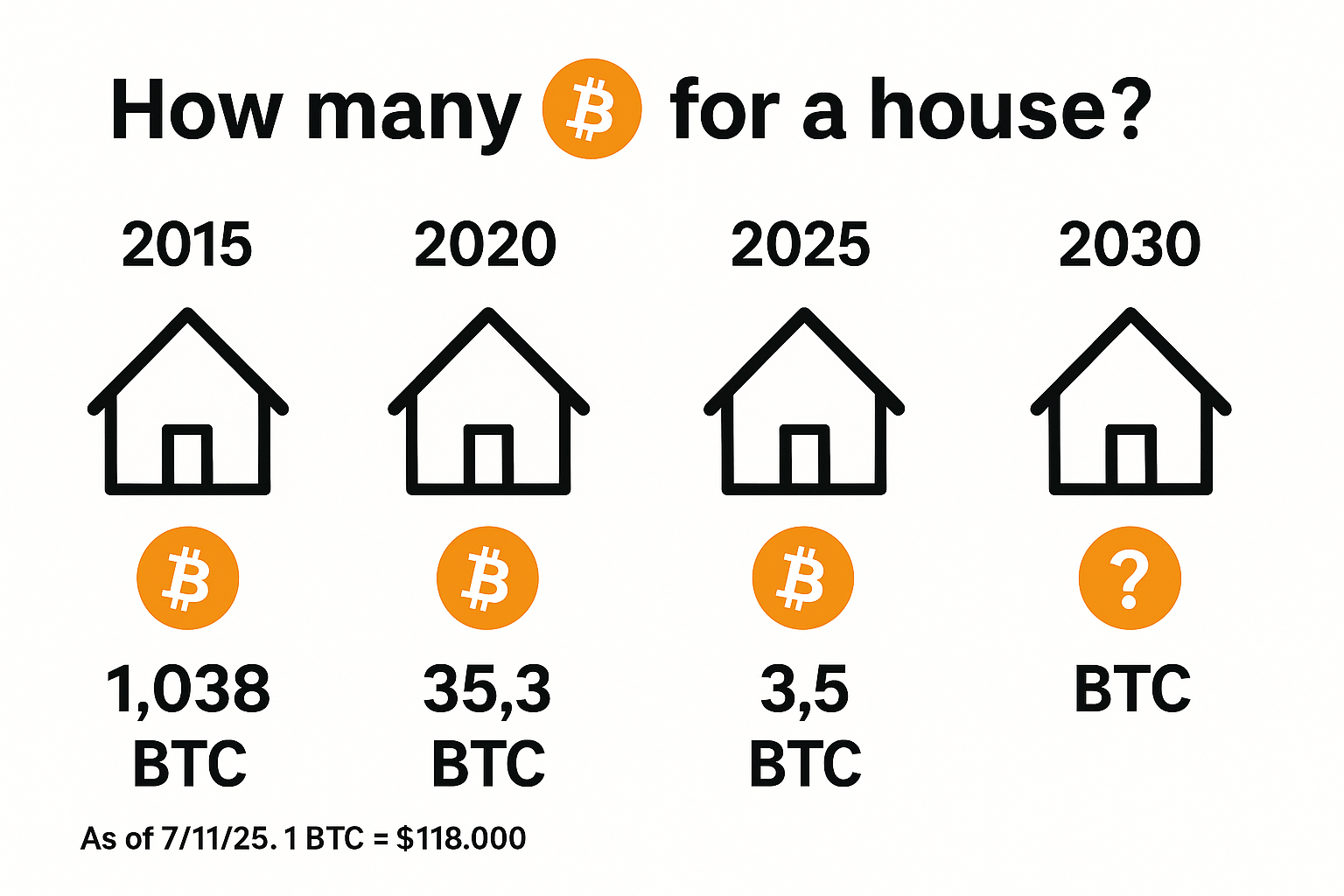

Why Assets Can Look “Cheaper” in Bitcoin Terms

Think about a home, a car, or a college education. In most fiat economies, these items get more expensive over time when priced in dollars or euros. Some of that is real—land scarcity, regulatory and labor costs, or demand growth. Some of it is simply monetary—more currency units exist, so nominal prices float up.

Now price the same asset in BTC. If bitcoin appreciates over long horizons, you need fewer satoshis (the tiny units of BTC) to buy the same house or car. The house didn’t get objectively cheaper to build; it just became cheaper relative to a stronger unit of account. That’s what people mean when they say Bitcoin increases purchasing power: not that everything magically costs less to produce, but that a savings held in a scarce, globally tradable asset can outpace inflation and productivity trends, compressing the BTC price of real-world goods.

Two design elements reinforce this:

- Halvings reduce new supply, creating cyclical supply shocks that historically coincided with major bull cycles. While not a guarantee, the rhythm channels attention and investment.

- Credible monetary policy—because everyone can audit the supply—builds long-term trust. The market isn’t constantly repricing the risk of political changes or sudden stimulus.

Fiat Money, Credit, and the Inflation Tailwind

Fiat currencies are designed to be elastic, supporting lending, employment, and crisis response. Central banks target inflation (often ~2%) to avoid deflationary spirals and to keep debt burdens manageable. Commercial banks create most of the money supply through lending. When credit expands, so does broad money.

The cost of this flexibility is that purchasing power tends to erode. Even “low and stable” inflation compounds: at 3% inflation, prices roughly double in about 24 years. Savers must continually reach for yield just to break even after inflation and taxes. In many periods, wages lag prices, and assets like real estate or equities run ahead—great if you own them, painful if you don’t.

Money printing during crises accelerates this effect. When central banks add reserves and governments run large deficits funded by bond issuance, the system gains liquidity. That support can be vital to avoid depression, but it also pushes up nominal asset prices and eventually consumer prices, diluting the buying power of cash balances.

Measured Over Years, Not Weeks

Bitcoin is volatile. Over short windows, it can fall 50% or more. If you zoom out, though, the long-run trend since inception has been rising purchasing power. This is typical of a new monetary asset: thin liquidity, reflexive narratives, and cycles around adoption milestones.

For the argument “Bitcoin makes assets cheaper” to hold, you have to think in multi-year horizons. Over a decade, several forces compound:

- Growing holder base—from retail to institutions and, in some cases, sovereigns.

- Expanding infrastructure—custody, ETFs in some jurisdictions, payment rails, and capital markets around BTC.

- Relative scarcity—as more people compete for a fixed pie, the unit price trends up.

If you saved a slice of your income in BTC across cycles, your capacity to purchase large assets may rise dramatically compared to saving in cash—on average and over time. The flipside: timing risk is real; buying near a euphoric peak and needing funds during a drawdown can negate those gains. Scarcity doesn’t cancel volatility.

Why a Fixed Supply Protects Savers

A fixed supply currency favors savers. When your money cannot be diluted, your share of total purchasing power in the system remains intact unless you spend it. In fiat, even cautious savers must become investors, constantly choosing between risk assets to outpace inflation. That’s not neutral; it forces financialization.

Bitcoin’s proposition is minimalist: hold a slice of a scarce digital good that no one can debase. If adoption grows, you ride the tailwind. Even if adoption plateaus, the baseline is non-dilution—you aren’t losing ground to money supply growth. That’s a dramatically different deal than holding cash in an inflationary regime.

Common Critiques—and Responses

“Deflation makes people hoard and economies stall.”

Mild, productivity-driven deflation is normal in many tech sectors: your phone or cloud compute gets better/cheaper. People still buy them because utility rises. With Bitcoin, spending vs. saving depends on personal preference and opportunity cost. You’ll spend BTC if the good or investment you’re buying is expected to outperform BTC, or if you simply value the utility now. And you can still price and settle in local currency while saving in BTC.

“Credit markets can’t function on a fixed supply.”

Credit existed under gold standards with far more rigid monetary bases. What changes is the discipline of lenders and borrowers. In a BTC-anchored environment, maturity transformation and risk pricing need to be tighter, and leverage cycles should be less explosive. Layered systems (e.g., credit built on BTC collateral) can still exist, but with clearer bounds.

“Volatility makes bitcoin unusable as money.”

Volatility is a symptom of monetization. As market depth grows, derivatives mature, and adoption broadens, volatility tends to decline. In the meantime, many treat BTC primarily as a savings asset rather than a day-to-day unit of account, using stablecoins or fiat for spending and lightning/other rails for fast settlement when needed.

Putting It All Together

- Bitcoin’s fixed supply creates a structural bid for purchasing power over long horizons as demand compounds. The same house, car, or basket of goods often becomes cheaper when priced in BTC across cycles.

- Fiat money creation provides needed flexibility but dilutes purchasing power; inflation—quiet or loud—taxes savers and pushes capital into risk assets just to preserve value.

- The result is a growing gap: assets typically rise in nominal fiat terms while declining in BTC terms during secular uptrends. That’s what “Bitcoin makes assets cheaper” really means.

None of this guarantees straight-line gains. Bitcoin’s path is jagged, and future policy, regulation, and technology shifts matter. But if its core promise—credible, unchangeable scarcity—continues to attract savers, the long-term effect is simple: each unit of bitcoin claims a larger share of the world’s value, and your savings buy more life rather than less.

Bitcoin vs Fiat Money — Why Scarcity Matters

At its core, Bitcoin’s appeal comes from the contrast with traditional government money (fiat):

- Bitcoin has a hard cap of 21 million coins — no central authority can print more. That scarcity is built into its code.

- Fiat currencies like USD can be created at will by governments and central banks through debt financing and policies like quantitative easing. That expands the money supply.

- When more money chases the same amount of goods/services, prices rise → inflation → cash loses purchasing power over time.

Bitcoin is attractive as a store of value because its supply is fixed and predictable — unlike cash, which can be diluted.

🏦 2. U.S. National Debt & Monetary Expansion

The U.S. national debt has surpassed $38 trillion, and rising deficits often lead to debate about monetary policy, inflation, and financial stability.

Why does that matter for Bitcoin?

- High debt pressures central banks to keep interest rates low or undertake “money printing” (i.e., quantitative easing / debt monetization) to support government spending and avoid market stress.

- This increases the money supply — which historically erodes the value of fiat over long periods.

- Bitcoin offers a non-state, non-inflatable asset that cannot be debased in the same way — a reason both institutions and wealthy individuals are considering it as a hedge.

Some money managers even argue that U.S. debt dynamics strengthen Bitcoin’s narrative as a scarcity asset.

🏢 3. Why Institutions & Rich Investors Buy Bitcoin

There are a few big reasons:

📌 A. Diversification & Risk Management

Large institutions are adding Bitcoin to portfolios not just as speculation, but as a diversification tool because:

- Bitcoin historically has had low correlation with stocks and bonds.

- It offers a different risk/return profile than traditional financial assets.

📌 B. Inflation Hedge (Digital Gold Thesis)

Many investors view Bitcoin like digital gold: a potential store of value when currencies weaken or inflation rises. Bitcoin cannot be inflated the way fiat can.

📌 C. Strategic Reserves (Government & Corporate)

Some policymakers and corporate treasurers are exploring Bitcoin as a strategic reserve asset to diversify away from fiat and traditional reserves like bonds or gold — similar to how countries hold commodities or foreign currency reserves.

Even if it won’t “pay off the debt,” holding Bitcoin can be seen as a long-term hedge against currency debasement.

📉 4. The Cantillon Effect — Why the Rich Get Richer

The Cantillon Effect explains how money creation benefits certain groups more than others:

- New money enters the economy at specific points (e.g., banks, big financial institutions) before it spreads to the broader public.

- Those closest to the “money printing tap” get to use the new money first — buying assets, investing, and benefiting from rising prices.

- By the time the newly created money filters out to workers and savers, prices of goods and assets have already jumped, so ordinary people are left with diminished purchasing power.

This dynamic tends to:

- Boost asset prices (stocks, real estate, crypto) — which disproportionately helps wealthier individuals who own these assets.

- Weaken the value of cash savings — which disproportionately hurts wage earners and those with fewer assets.

Hence the sense that money printing enriches the asset-rich and squeezes cash-poor households.

Bitcoin’s advocates argue it could help counter this effect by providing an alternative to inflationary fiat — but it’s not a magical solution: Bitcoin is still volatile and doesn’t replace the existing monetary system outright.

🧠 5. Summing It Up in Plain Terms

Why governments, central banks, and the wealthy are looking at Bitcoin:

✔️ Bitcoin offers a fixed-supply asset in a world where fiat currencies can be expanded at will.

✔️ Institutional investors see it as portfolio diversification and a potential inflation hedge.

✔️ Some policymakers explore it as a strategic reserve to diversify national assets.

✔️ High sovereign debt and expansive monetary policy feed narratives of currency debasement, reinforcing Bitcoin’s appeal.

✔️ The Cantillon Effect explains why new money tends to benefit wealthy, asset-owners more than ordinary citizens — deepening inequality.

🧩 Important Reality Check

Bitcoin doesn’t magically fix national debt, and its price and adoption are volatile and uncertain. Economists agree that fiscal policy and structural reforms — not crypto — are the core solutions to long-term government debt issues.

But as a financial narrative and hedging tool, Bitcoin’s scarcity and decentralization are precisely why some powerful players are paying attention.